A New Market Demands a New Model

Grid-scale battery storage is becoming essential infrastructure in a more volatile and capacity-constrained power system. How GridCore is recalibrating to the investing environment of 2026

The Market Has Changed. So Have We.

The Nordic power system is entering a structurally new phase. Increasing volumes of variable renewable generation, accelerating electrification, and growing pressure on grid capacity are creating persistent demand for flexibility, fast response, and smarter utilisation of existing infrastructure. Battery Energy Storage Systems (BESS) are no longer just opportunistic market products; they are becoming indispensable parts of critical power system infrastructure.

But the capital markets have shifted too, and perhaps more abruptly. The investing environment of 2025 was already more demanding than the years before it. Tariff uncertainty triggered by US trade policy sent the S&P 500 down nearly 20% in seven weeks around April 2025¹, European gas storage entered the winter at historically low levels, and institutional investors across the board began repricing risk. Then, in early 2026, the situation became more acute.

The Iran conflict, which broke out in late February 2026, caused an immediate surge in Brent crude of 10 to13%² and pushed Dutch TTF gas benchmarks to over €60/MWh, nearly double pre-conflict levels³. The International Energy Agency described the resulting energy security situation as the greatest global challenge in the history of the modern oil market⁴. With the Strait of Hormuz effectively closed to normal traffic, roughly 20 million barrels per day of global oil flow came under threat⁵. The European Central Bank postponed planned rate cuts and revised its inflation forecast upward. UK inflation is now expected to breach 5% in 2026⁶. Economists are warning of recession risk in energy-import-dependent economies across Europe and Asia⁷.

At the same time, US trade and fiscal policy under President Trump continues to inject structural uncertainty into global capital markets. The average effective tariff rate reached 7.7% in 2025, the highest since 1947⁸. While the Supreme Court struck down the broadest IEEPA-based tariffs in February 2026⁹, a 10% global tariff remains in place, and the policy environment remains unpredictable. Investors globally are navigating a world in which US policy signals shift quickly, geopolitical risk is persistent rather than episodic, and inflation is unlikely to return to the low, stable levels that shaped investment frameworks for most of the 2010s¹⁰.

We are not positioning GridCore for a world that no longer exists. We are building for the investing environment of 2026 and beyond: higher costs, higher uncertainty, and a premium on assets that deliver real and visible returns.

This is the context in which GridCore's updated business plan has been developed. This article sets out the core elements of that recalibration.

From Project Developer to Industrial Platform

The most important strategic change is one of identity. GridCore is not positioning itself as a traditional project developer, nor as a financial fund. We are building an industrial platform for battery storage; one that develops, de-risks, finances, owns, and optimises BESS assets across their full operational lifetime.

This distinction matters. A project developer sells and moves on. A fund structures and distributes. An industrial platform does something more durable: it takes complexity and development risk, and converts them into de-risked, operational, and financeable assets. Then it stays engaged, optimizing commercial performance, managing investor reporting, and compounding operating know-how.

GridCore’s model is built around delivering de-risked, operational assets rather than simply originating projects.

Our value proposition rests on three pillars: the structural necessity of storage flexibility in the Nordic grid, an investor market that rewards clear structure and demonstrated execution over thematic storytelling, and a private markets environment where returns come from operational alpha - not passive market tailwinds.

How Investor Risk Preferences Have Shifted

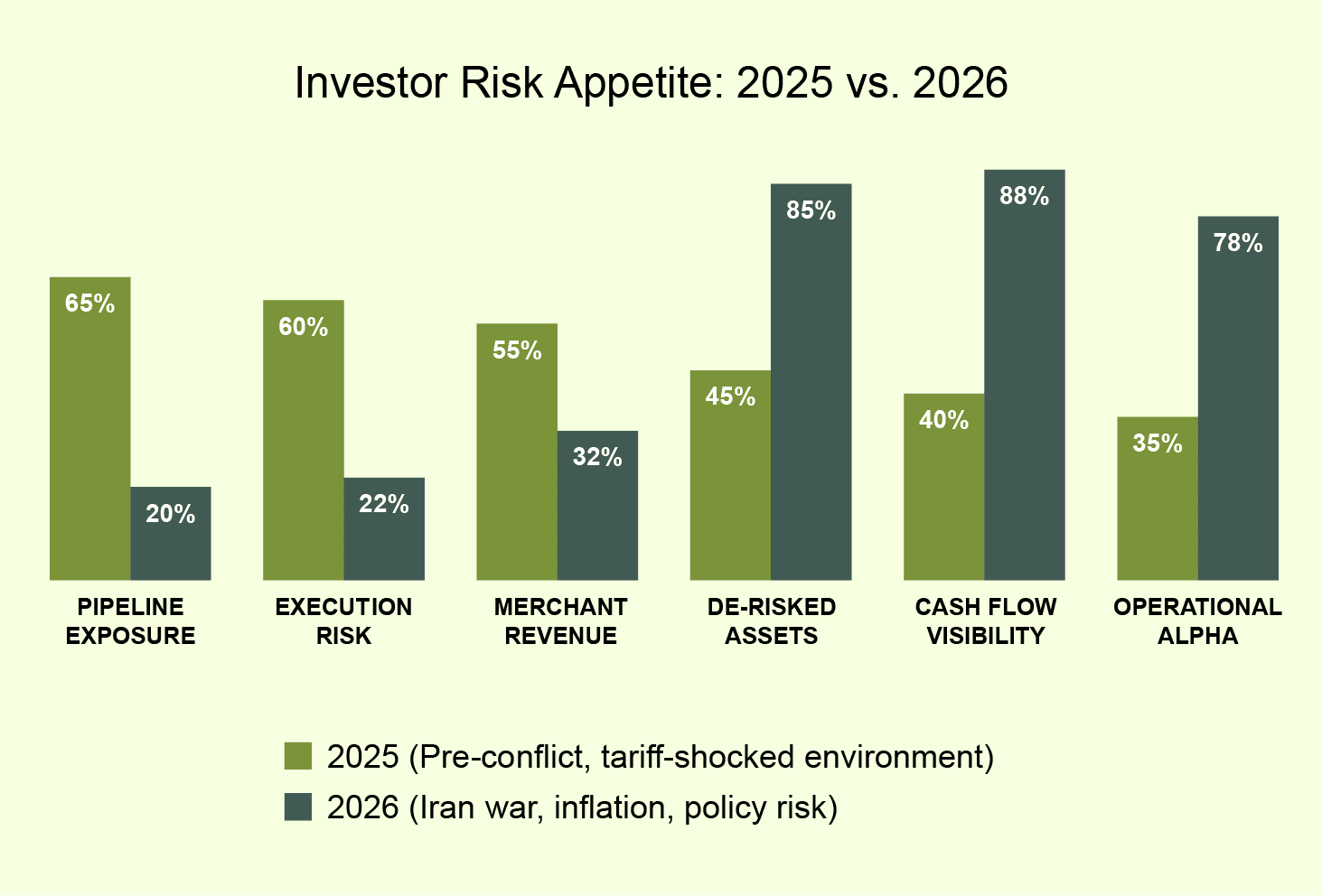

The chart below illustrates the shift in what institutional investors are prioritising today compared to 2025, before the full impact of the Iran conflict and the cumulative weight of US trade policy uncertainty. Appetite for raw pipeline exposure and early-stage execution risk has declined sharply. Demand for de-risked assets, operational transparency, and visible cash flow has increased significantly.

Figure 1: Indicative investor risk appetite shift across key dimensions, 2025 vs. 2026.

This shift directly informs how GridCore structures its capital raise and how it communicates with prospective investors. Broad pipeline narratives are being replaced by project clusters with clear timelines. Abstract upside is being replaced by modelled downside scenarios, sensitivity tables, and realistic paths to cash distributions.

A Multi-Stream Revenue Model Built for Alignment

GridCore's updated business model is designed to ensure that the company is compensated for every distinct form of value it creates, and that its economics remain aligned with investor outcomes at every stage.

Revenue Stream | GridCore Gets Paid For | Strategic Function |

Development Premium | Origination, site securing, grid dialogue, project maturation to investment-ready standard. | Ensures payment for early-stage expertise and de-risking before external capital commits. |

Delivery Premium | EPC oversight from investment decision through to Commercial Operation Date (COD). | Reflects GridCore absorbing execution risk and delivering a fully operational asset. |

Bridge Capital Fee | Capital deployed in development and construction phases ahead of institutional investor entry. | Compensates for time-value of capital and financing risk during the highest-uncertainty period. |

Retained Equity / Promote | Long-term upside through a 5% co-investment stake and performance-based returns above agreed hurdles. | Aligns GridCore economics with investor outcomes – rewards actual value creation, not fees alone. |

SLA / Operations | Ongoing asset management, investor reporting, and commercial optimisation across the project lifetime. | Generates recurring revenues and underpins the operating alpha differentiator. |

Table 1: GridCore's five revenue streams and their strategic rationale.

Pricing transparency is a core design principle, and early revenue is a commercial necessity, not a preference. GridCore funds all capital expenditure and operating costs from project initiation through to Commercial Operation Date, a period that typically spans 12 to 18 months. During that window, no external investor capital is in place. GridCore carries the full financial exposure: site costs, grid connection fees, engineering work, permitting, and all associated overhead. The development premium, delivery premium, and bridge capital fee are therefore not discretionary line items that can be deferred or renegotiated away, they are the mechanism by which GridCore is compensated for real capital at risk, deployed early, and recovered only when a project reaches the point at which it becomes investable for others. Each fee must be clearly articulated as payment for a specific and tangible contribution: de-risking the asset, funding the build, and delivering a project that is operational and bankable. This framing is not in tension with investor interests - it is the honest foundation for a durable partnership.

Institutional capital increasingly favours assets supported by operational transparency, structured reporting, and visible performance data.

Capital Strategy: Selective, Structured, and Credible

Fundraising today is slower, and investors are more demanding. GridCore's capital strategy reflects this reality. Rather than pursuing broad-based fundraising on the strength of a pipeline narrative, we are prioritising project clusters with clearly defined risk profiles, club deals with strategic or industrial investors who understand the sector, and a clean separation between development capital and long-term operational capital.

Our investor materials are being standardised to reflect what sophisticated LPs actually need: risk allocation frameworks, downside scenarios, sensitivity analyses, and a credible, evidence-based path to cash flow and capital recycling. We are targeting a first project cluster close with external capital during 2026, establishing a reference transaction and a repeatable model.

The goal is not to tell a compelling story. It is to build a documented, repeatable transaction model that earns investor confidence through execution, not promises.

Five Priorities for 2026

The following table sets out GridCore's five near-term workstreams and their intended outcomes. These are not aspirations; they are the operational commitments that underpin our investor proposition.

Work Stream | Priority Action | Intended Outcome |

Positioning | Finalise one clear investor narrative and a standardised investor pack. | Higher credibility, faster due diligence, and quicker capital decisions. |

Pipeline | Rank projects by market access probability, COD likelihood, and profitability. Secure lease agreements immediately. | Improved capital discipline and lower risk of misallocation. |

Capital | Close first project cluster with external capital on a clear structure during 2026. | Establish reference transaction and a documented, repeatable model. |

Operations & KPIs | Implement KPI governance for availability, revenue per MW, CAPEX, CFADS, and DSCR. | Build operating alpha and strengthen investor follow-up capacity. |

AI & Data | Develop internal tools for commercial optimisation and reporting. | Better decision-making, higher realised returns, and scalability. |

Table 2: GridCore's five strategic workstreams and intended outcomes for 2026.

Our platform now systematically uses AI and data tools for commercial optimisation and investor reporting, reflecting the evolving competitive landscape. As dispatch strategies grow more complex and market conditions more volatile, the ability to analyse, act, and report in near-real time becomes a material source of operating alpha.

System Value: A Responsible Claim

GridCore operates within a broader system, and we believe it is important to be precise about the system value our projects create. Battery storage can contribute to better utilisation of existing grid infrastructure, reduce or defer the need for costly new transmission investment, and over time dampen cost pressures that would otherwise materialise as higher grid tariffs.

We do not claim that our projects will directly reduce network tariffs. What we can say with confidence is that well-located, well-operated BESS assets make the power system more efficient, more resilient, and better equipped to absorb the variability that comes with the energy transition. That is not marketing language, it is a factual description of what grid-scale storage does.

Conclusion

GridCore's updated business plan is calibrated to the world as it is - not as it was. The market is more selective. Investors want different kinds of risk. The assets that attract capital in 2026 are those that combine operational credibility, structural clarity, and a demonstrable path to cash flow.

We believe GridCore is well positioned to be exactly that kind of platform. We are not asking investors to price in optionality. We are asking them to recognise the value of de-risked, operational, and optimised infrastructure assets - built, owned, and managed by a team with the execution capability to deliver.

We look forward to continuing the conversation.

² Goldman Sachs, “How Will the Iran Conflict Impact Oil Prices?,” March 3, 2026

³ Wikipedia, “Economic impact of the 2026 Iran war,” accessed April 22, 2026

⁴ International Energy Agency, “Oil Market Report – March 2026,” March 12, 2026

⁵ Goldman Sachs, “How Will the Iran Conflict Impact Oil Prices?,” March 3, 2026

⁶ European Central Bank, “Monetary policy decisions,” March 19, 2026 See also Wikipedia, “Economic impact of the 2026 Iran war”

⁷ Charles Schwab, “Iran War: Ceasefire Offers Relief, Not Resolution,” April 10, 2026

⁸ Tax Foundation, “Tariff Tracker: 2026 Trump Tariffs & Trade War by the Numbers,” April 2026

⁹ Tax Foundation, “Supreme Court Strikes Down President Trump’s Tariffs,” February 20, 2026

¹⁰ J.P. Morgan Global Research, “US Tariffs: What’s the Impact?,” April 15, 2026 and Morgan Stanley Wealth Management, “Iran War Oil Shock: Stock Market Impacts,” March 18, 2026