Merchant BESS: Risk Premium Compression, Leverage, WACC and Valuation Uplift Across Project Stages

Executive summary. Pure merchant Battery Energy Storage Systems (BESS)—i.e., projects without long-term PPAs or contracted revenue floors—are priced primarily on the basis of (i) project-stage risk (development vs. construction vs. operating) and (ii) financial structure (leverage). As projects mature from Full Risk (development) to RTB (ready-to- build) to COD (commercial operation date), discrete execution risks are progressively resolved and replaced by predominantly market and operational risk. This risk resolution compresses required equity returns, reduces WACC, and mechanically increases valuation for a given cash-flow stream. The effect is amplified when the investor base broadens to include lower-cost ‘core’ infrastructure capital at COD.¹

Definitions and scope

This paper focuses on merchant BESS projects (no PPAs, no fixed tolling). We use three standard project stages: (a) Full Risk (development-stage, pre-RTB), (b) RTB (permits and grid secured; construction pending), and (c) COD (operational asset). We analyse leverage at 25%, 50% and 75% (defined as D/(D+E)). The return levels presented are illustrative midpoints aligned with typical investor discussions and market ranges for merchant flexible infrastructure, and are intended for comparative analysis rather than forecasting.²

Why risk declines as projects mature

Risk declines with maturity because the dominant risk factors shift from binary, idiosyncratic execution events to more continuous, diversifiable operating variability. In Full Risk, value can be impaired by discrete outcomes: a permit is delayed or denied; grid connection terms change; land agreements fail; capex inflates; equipment lead times slip; or financing is unavailable on workable terms. These are ‘event risks’ with fat-tailed outcomes and limited ability to hedge. In real-options terms, development resembles a sequence of irreversible investments under uncertainty, where investors demand a high hurdle to compensate for downside asymmetry and capital at risk.³

At RTB, a large fraction of the event risk has been resolved: key permits, land rights, and grid access have typically been secured. The remaining risk is dominated by construction execution and procurement—still material, but narrower in scope and better mitigated through EPC contracting, liquidated damages, performance guarantees, and contingency budgeting. Empirical studies of infrastructure delivery show that cost overruns and schedule delays are common and value-destructive, which supports a persistent RTB premium versus COD.⁴

At COD, the binary execution risks are largely gone: the asset is built, commissioned, and producing. Risks become primarily (i) market risk (reserve prices, intraday volatility, ancillary services conditions), (ii) operational risk (availability, degradation, warranty performance), and (iii) regulatory ‘rules-of-the-game’ risk. While merchant cash flows remain volatile, the uncertainty is more quantifiable via historical price distributions and operational KPIs. In asset-pricing terms, a greater share of the risk is systematic (market- linked) rather than idiosyncratic execution, which supports a lower required return.⁵

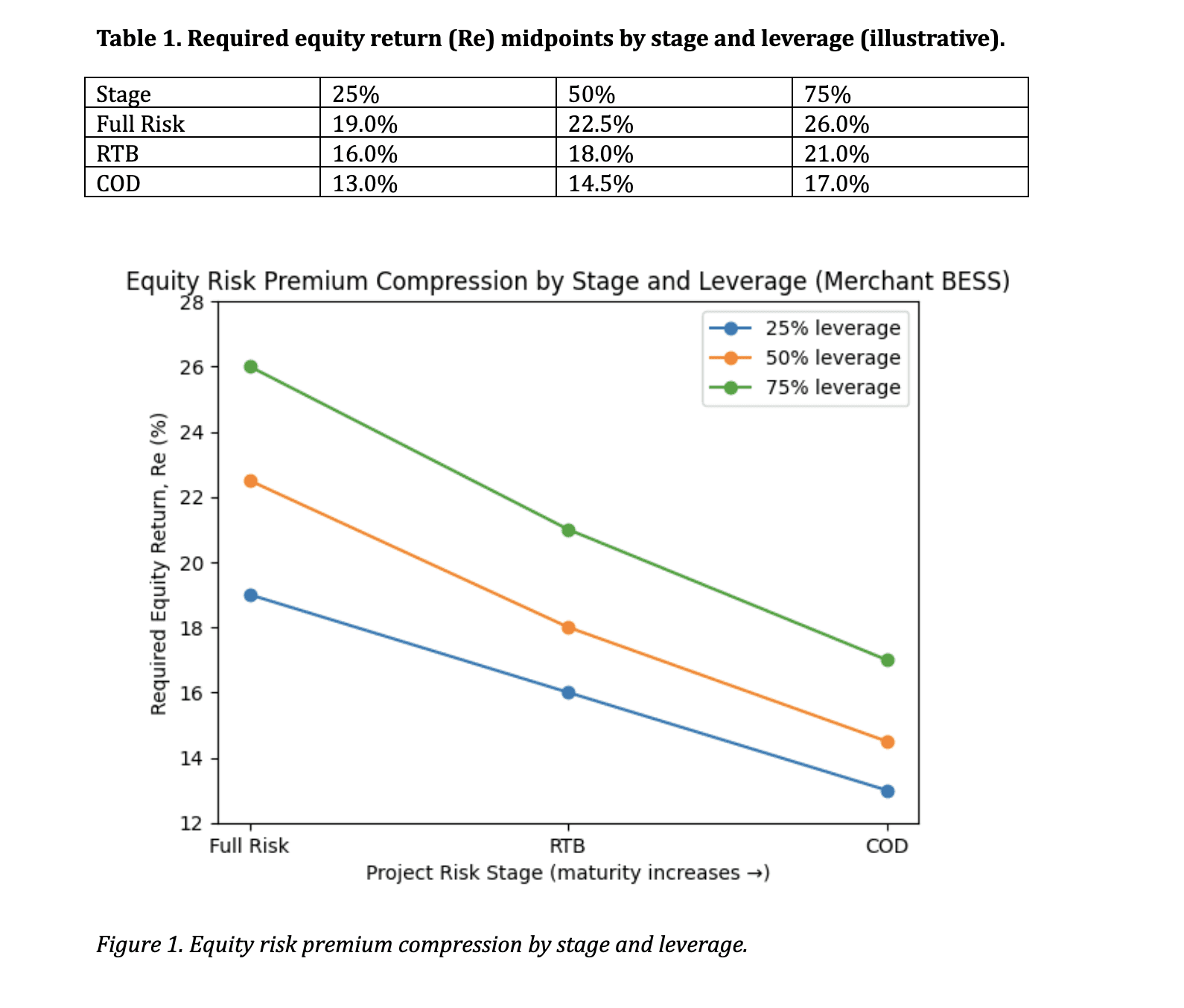

Required equity returns by stage and leverage (merchant, no PPA)

Table 1 summarises illustrative midpoint required equity returns (Re) by stage and leverage. The pattern is intuitive: (i) moving from COD → RTB → Full Risk increases Re due to execution/event risk; and (ii) increasing leverage increases Re because equity becomes a residual claim with higher volatility and higher probability of impairment under adverse revenue or delay scenarios. At high leverage (e.g., 75%), the profile increasingly resembles private equity-style risk rather than traditional infrastructure.⁶

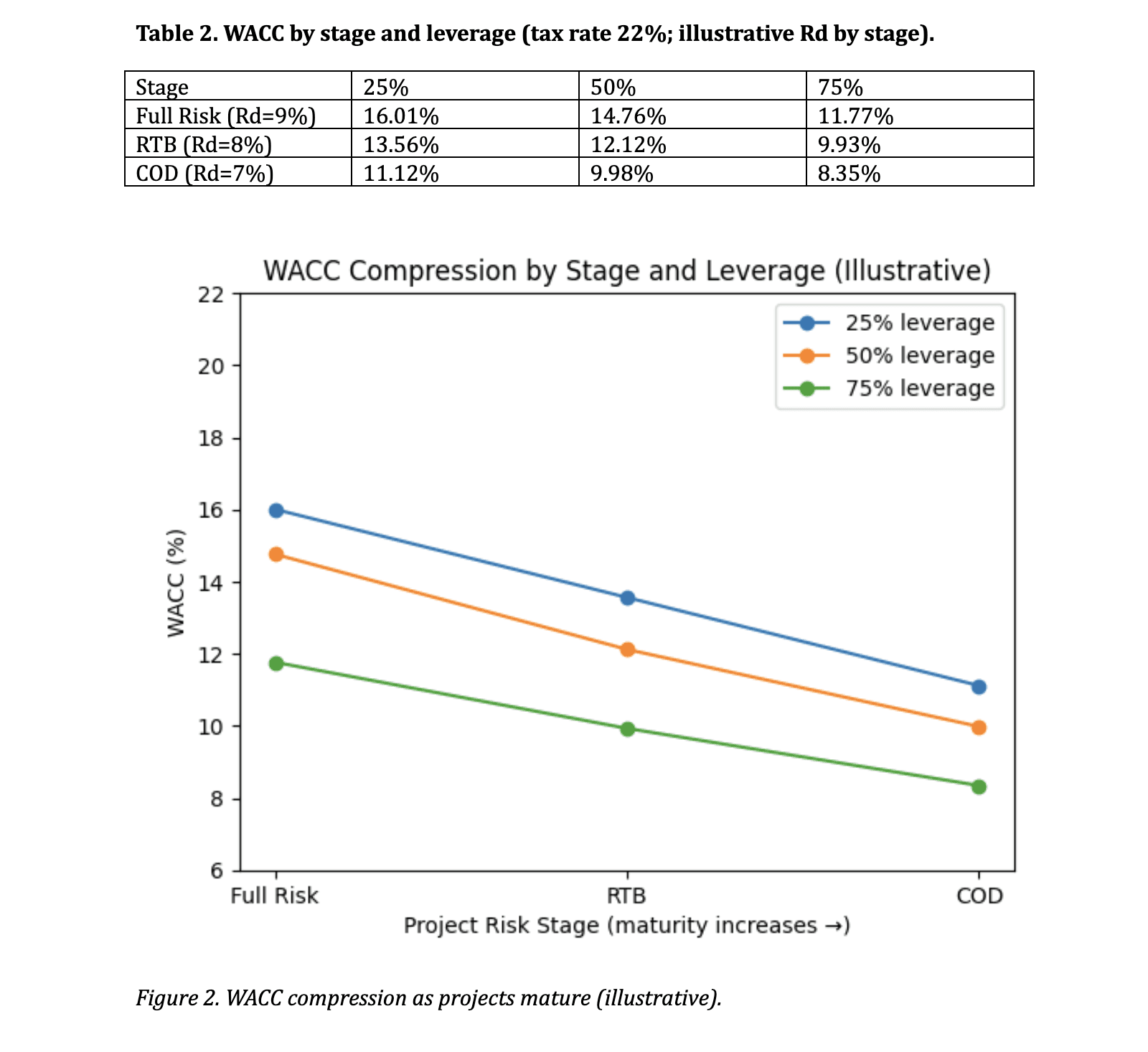

WACC: calculation framework and stage-driven compression

For investment valuation and pricing, the relevant discount rate is typically a form of WACC.

We use the standard definition: WACC = (E/(D+E))·Re + (D/(D+E))·Rd·(1−T), where Re is required equity return, Rd is cost of debt, and T is the corporate tax rate.⁷ In merchant assets, Re usually drives most of the variation across stages because execution risk and market uncertainty are priced primarily in equity. Debt cost also improves with maturity as lender risk declines. In our illustration we assume Rd declines from 9% (Full Risk) to 8% (RTB) to 7% (COD), reflecting improved bankability, lower completion risk, and tighter covenants at later stages.

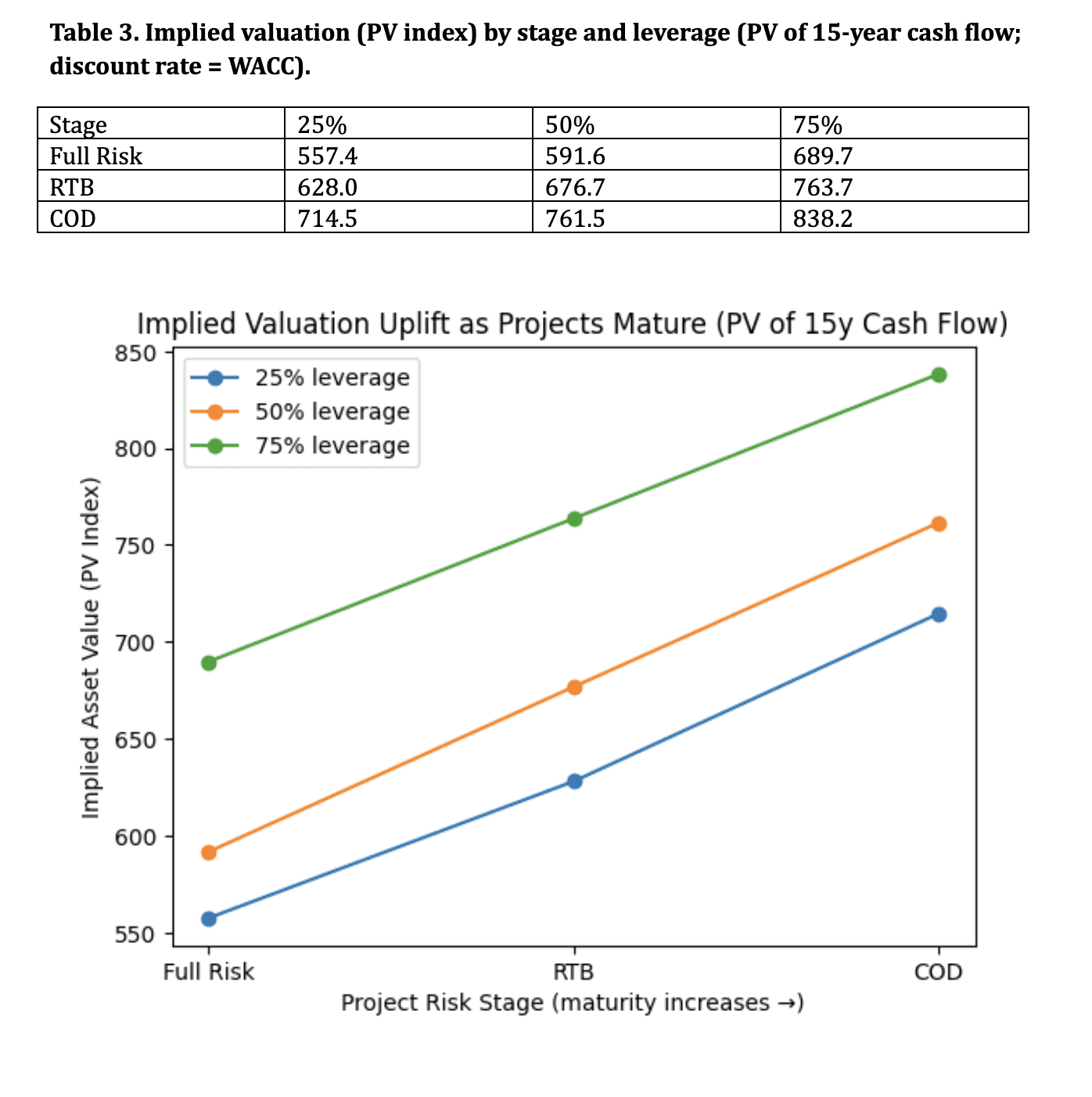

Valuation uplift: why later-stage assets are worth more

Lower WACC increases valuation mechanically by increasing the present value of expected future cash flows. Importantly, the relationship is nonlinear: a reduction in WACC from, say, 18% to 14.5% increases PV by more than a proportional amount, particularly for longer duration cash flows. In addition to purely mathematical discounting, later-stage assets often attract a broader set of investors (core/core+ infrastructure funds, long-term capital, yield oriented vehicles). This demand expansion can further compress required returns, raising valuation multiples at exit.⁸

To illustrate the mechanical effect, we value an identical 15-year cash-flow stream (constant annual cash flow index of 100) under each WACC scenario. The implied PV Index is not a forecast of absolute value; it is a comparable measure that isolates the discount-rate effect.

Table 3 shows the valuation uplift across stages for 25%, 50%, and 75% leverage.

Valuation uplift from Full Risk to COD (mechanical discount-rate effect): 28% at 25% leverage, 29% at 50% leverage, and 22% at 75% leverage (based on the illustrative WACC assumptions above). This is the economic basis for development premium capture: by taking development and construction risk off the table, sponsors can sell into a lower cost-of-capital market at COD.

Implications for investment structuring and sponsor economics

For investors, the key decision is whether they are being compensated for the specific risk bundle they bear. A COD entry should be priced on operating and market risk; RTB should include a construction premium; Full Risk should include permitting, grid, and execution premia. For sponsors, the development strategy should target ‘risk-to-value’ conversion: invest capital and capability in resolving discrete risks, then monetise that de-risking through (i) lower required returns and (ii) a broadened capital buyer universe. This is particularly relevant in merchant BESS where cash-flow volatility persists, but execution risk can be largely eliminated before syndication.

7. Mathematical appendix (investment-useful)

WACC formula: WACC = wE·Re + wD·Rd·(1−T), where wE = E/(D+E), wD = D/(D+E). Equity return Re can be mapped to CAPM: Re = Rf + β·(Rm−Rf) + α, where α may include illiquidity and project-specific premia.⁹ In practice, merchant infrastructure often uses build-up methods rather than pure CAPM due to limited public comparables and nonlinear risk. Importantly, as projects mature, idiosyncratic execution risk declines, which reduces α and potentially β, leading to lower Re and lower WACC, thereby increasing valuation.

¹ Real-options and staged investment logic implies higher hurdles where downside is asymmetric and investments are irreversible; see Dixit & Pindyck (1994).

² Market midpoints are illustrative and intended for comparative use; in practice they vary by jurisdiction, revenue stack, and contracting package.

³ Dixit, A.K. & Pindyck, R.S. (1994). Investment Under Uncertainty. Princeton University Press.

⁴ Flyvbjerg, B. (2014). What You Should Know About Megaprojects and Why. Project Management Journal; and broader cost-overrun literature.

⁵ Sharpe, W.F. (1964). Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. Journal of Finance.

⁶ Modigliani, F. & Miller, M.H. (1958; 1963). The Cost of Capital, Corporation Finance and the Theory of Investment; and corporate taxes and leverage.