Why Norway Needs BESS in a Hydropower Country

A strategic perspective on battery storage in the Norwegian power system

Executive Summary

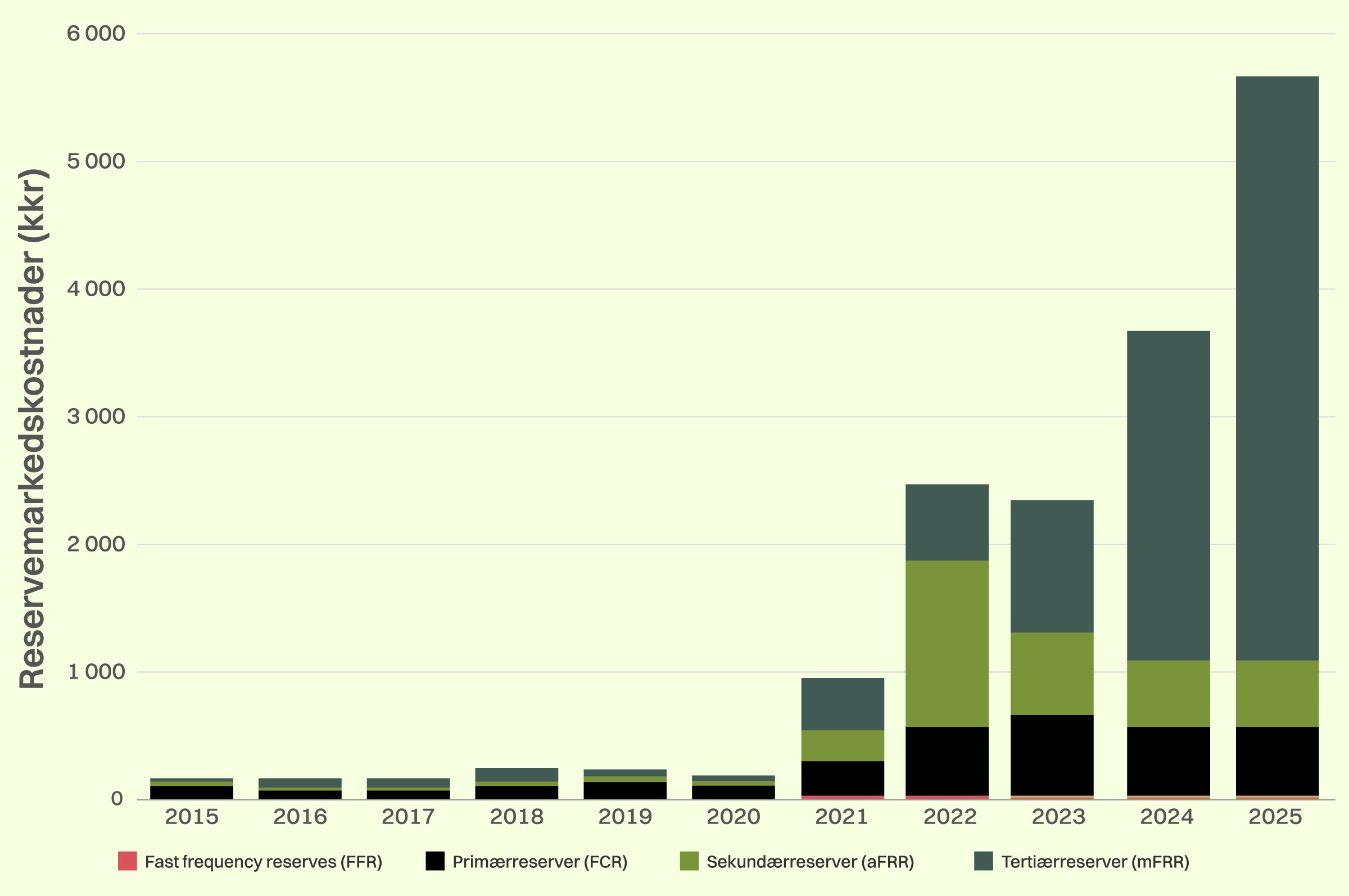

Norway’s power system has long been balanced cheaply by dispatchable hydropower, but tighter European integration, stricter balancing requirements and rising volatility pushed Statnett’s reserve costs to NOK 5.6 billion in 2025 [1]. These costs are structural: hydropower prices reserve-market participation at its opportunity cost, not at its low physical cost of delivery, so reserve-market so prices will stay persistently high.

Battery storage (BESS) addresses this directly. With near-zero marginal cost and response that exceeds Statnett’s technical requirements, it complements hydropower rather than replacing it. As BESS volume enters the market, it will eventually lower reserve-market prices and reduce system costs, eventually reaching levels close to the marginal cost of new BESS projects.

For investors, that same shift creates a time-limited opportunity. Prices today are still set by higher-cost hydropower, capex has fallen, and Statnett is gradually opening the markets to new participants. Early movers can stack revenues across the reserve and energy markets and capture this spread before new capacity saturates it and prices fall toward BESS’s own marginal cost. For well-sited, prequalified projects, a double-digit IRR is achievable over five to ten years and with a limited number of viable sites and constrained grid capacity, the first-mover advantage is real. The window is open now.

How the Norwegian power system is balanced today

The Norwegian power system is dominated by dispatchable hydropower, with dispatchable capacity of 26,3-33,3 GW. Historically, the system has had a large surplus of both energy (15TWh) and power capacity (2,6GW) [2], and the distributed, dispatchable hydropower, combined with seasonal and relatively stable demand, has made the system simple and inexpensive to balance.

In recent years, this system has come under pressure. Closer integration with Great Britain and continental Europe, more unpredictable generation and consumption patterns, and increased price volatility in the wake of Russia’s invasion of Ukraine impose stricter requirements on the balancing of the integrated Nordic power system. To meet this new reality, the Nordic system operators (Statnett, Svenska kraftnät, Fingrid, and Energinet) have developed a new framework through the Nordic Balancing Model (NBM) [3]. The framework comprises the fast frequency reserve (FFR), new technical requirements for primary reserves (FCR), an activation market for tertiary reserves (mFRR), and planned integration with the European platforms PICASSO and MARI for secondary (aFRR) and tertiary (mFRR) reserves, respectively.

Together, these developments challenge the way the power system has been operated, and this is reflected in the rising reserve costs Statnett has faced in recent years, reaching NOK 5.6 billion in 2025 [2].

Why dispatchable hydropower alone does not deliver cost-optimal balancing

Dispatchable hydropower will secure balance in the Norwegian power system for a long time to come. Hydropower does, however, have certain properties that stand in the way of cost-optimal balancing.

The most important is opportunity cost. A reservoir hydropower producer must continually weigh whether to use the water now or save it for a later, more profitable moment; this value is known as the water value, and it represents the producer’s opportunity cost. This feeds directly into the reserve markets: in high-price hours, the producer must choose between generating at full capacity in the energy market or holding capacity back to offer upward regulation. Reserve market prices then reflect the forgone generation revenue - resulting in high upward-regulation prices. In low-price hours, the opposite applies; to have something to regulate down from, the producer must generate below the water value and seeks to recover the loss in the reserve market. In both cases, it is the water value, not a low physical cost of delivery, that drives the price.

On top of this come two more technical limitations. Statnett has tightened the requirements for the physical delivery of system services, and many older hydropower plants that deliver system services today are not built to meet them [4]. At the same time, reserves are activated more frequently, and producers must price mechanical wear into their bids. Both factors push prices up further.

Taken together, these factors imply that reserve prices are driven by opportunity costs rather than marginal costs. This not only pushes prices upwards, but also creates a structural demand for alternative flexibility providers. Battery storage, which is not subject to water value considerations or continuous production requirements, is particularly well positioned to capture this role.

Why BESS is the answer

BESS is the most flexible asset in the power system, and it complements the very capabilities hydropower struggles to deliver. Fast, precise, and stable power delivery that exceeds Statnett’s technical requirements. No mechanical wear - only gradual degradation of the battery cells’ storage capacity as a function of cycling and age. Marginal cost near zero once capex is in place. A system built on hydropower and BESS is robust and cost-effective.

The socioeconomic implications

The most important argument for BESS in Norway is economic: lower system operating costs, which reduce the grid tariff for everyone. Hydropower’s opportunity cost is a structural feature, and without more, and different types of flexibility, we expect the reserve market costs will remain high. Bringing more and different flexibility into the power system would result in:

Lower clearing prices in the reserve markets as volume enters at lower marginal prices

Increased competition in markets that have long been dominated by a small number of hydropower players

Better utilization of hydropower within the power system - peak load, seasonal storage, and export

The Norwegian BESS investment case

Compared with neighboring countries, there is little installed BESS capacity in Norway. This is because BESS investments here have historically been somewhat less attractive than in surrounding areas, driven by lower overall volatility and a more cautious opening of the reserve markets by Statnett.

Still, the Nordic market design suits a flexible asset like BESS: revenues are stacked across the reserve products (FFR, FCR-N, FCR-D, aFRR, and mFRR) alongside the day-ahead and intraday energy markets, as operators elsewhere in the Nordics already demonstrate. The combination of cost-efficient BESS and a gradual opening of the reserve markets creates an investment opportunity in Norway; we estimate that 500–1,000 MW of BESS in strategic nodes over the next five to ten years.

Timing is, however, critical. Early movers will be able to capture high reserve-market prices, set by hydropower, while late projects will enter a saturated market with prices closer to BESS’s own marginal cost. In addition, there are only a limited number of viable sites and with increasing electrification and strain on the grid capacity, there is a genuine first-mover advantage on the site acquisition as well. For well-sited, prequalified projects with market access, a double-digit IRR is achievable over five to ten years, though returns are sensitive to grid-connection cost, regulatory changes, and operational optimization.

The wider transition and conclusion

Beyond present-day balance, this is about building a robust, cost-effective system for the future. Non-dispatchable generation is expanding across Europe, and Norway is exposed to the resulting volatility through market integration. The new dynamics suit storable hydropower plus batteries: BESS contributes the flexibility needed for short-term balancing, while hydropower is reserved for delivering large energy volumes and seasonal storage.

Hydropower will remain the foundation of Norwegian power supply, but solving every balancing need with it is expensive and strategically weak. For regulators and Statnett, the task is to align market design, prequalification, and grid-connection regimes with BESS’s true value; for investors, it is an infrastructure asset deserving rigorous assessment of location, prequalification, counterparty risk, and operational competence. The window is open now, and those who position themselves before the markets saturate and capital costs normalize upward will hold a clear advantage in the coming decade.